.jpg)

What is Bitcoin Mining?

One of the fundamental questions many people have about Bitcoin revolves around the tokens themselves. Questions about its value, security and history, all eventually lead to one place: Where do bitcoins come from?

While traditional money is created through (central) banks, bitcoins are “mined” by Bitcoin miners: network participants that perform extra tasks. Specifically, they chronologically order transactions by including them in the Bitcoin blocks they find. This prevents a user from spending the same bitcoin twice; it solves the “double spend” problem.

Skipping over the technical details, finding a block most closely resembles a type of network lottery. For each attempt to try and find a new block, which is basically a random guess for a lucky number, a miner has to spend a tiny amount of energy. Most of the attempts fail and a miner will have wasted that energy. Only once about every ten minutes will a miner somewhere succeed and thus add a new block to the blockchain.

This also means that any time a miner finds a valid block, it must have statistically burned much more energy for all the failed attempts. This “proof of work” is at the heart of Bitcoin’s success.

For one, proof of work prevents miners from creating bitcoins out of thin air: they must burn real energy to earn them. And two, proof of work ossifies Bitcoin’s history. If an attacker were to try and change a transaction that happened in the past, that attacker would have to redo all of the work that has been done since to catch up and establish the longest chain. This is practically impossible and is why miners are said to “secure” the Bitcoin network.

In exchange for securing the network, and as the “lottery price” that serves as an incentive for burning this energy, each new block includes a special transaction. It’s this transaction that awards the miner with new bitcoins, which is how bitcoins first come into circulation. At Bitcoin’s launch, each new block awarded the miner with 50 bitcoins, and this amount halves every four years: Currently each block includes 12.5 new bitcoins. Additionally, miners get to keep any mining fees that were attached to the transactions they included in their blocks.

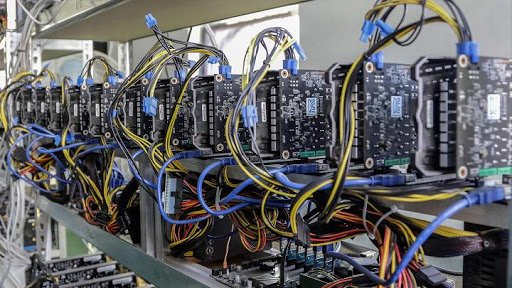

Anyone can become a Bitcoin miner to try and earn these coins. However, Bitcoin mining has become increasingly specialized over the years and is nowadays mostly done by dedicated professionals with specialized hardware, cheap electricity and often big data centers.

To mine competitively today, you need to know what you’re doing, you must be willing to invest significant resources and time, and — last but not least — you need access to cheap electricity. If you have all of this, you too can give it a shot and become a Bitcoin miner.

Source:https://bitcoinmagazine.com/guides/what-bitcoin-mining/

BENEFITS OF MINING CRYPTOCURRENCY

Making Money – At the end of the day, cryptocurrency mining can be a very profitable process. If done correctly, cryptocurrency mining could even replace a full time job. So, one of the largest benefits associated with cryptocurrency mining is the money that you make in doing so.

You Always Have Something Of Value – One of the most common questions I get asked with regard to cryptocurrency is, “can cryptocurrency crash?” The answer is yes. In fact, in the past, some cryptocurrencies have fallen in value by more than 20% in a single day. However, a cryptocurrency miner uses high-end computers and other equipment. These pieces of technology tend to hold their value very well. So, even if the cryptocurrency you were working to mine happened to crash, you would still have value in the equipment that you used to mine the currency.

Cryptocurrency Cannot Be Stolen – Unlike the more commonly used forms of currency, it is theoretically impossible for cryptocurrency to be stolen. As a result, you can rest assured that the money you’re mining for is safe in your account.

Safer Than Faucets – Another commonly asked question I receive with regard to cryptocurrency is “are cryptocurrency faucets safe?” Faucets are websites and apps that run the mathematical equations for people, rather than them having to use their own equipment to mine them. However, while there are tons of cryptocurrency faucets that are safe, there are also plenty of scams out there. By mining cryptocurrency yourself, you’ll avoid faucet based scams.

You Are Your Own Boss – Once you get good at cryptocurrency mining, it’s possible to replace your day job with the process. In doing so, you become your own boss. You set your own hours and your own rules, giving you the ultimate level of freedom!

A Bet Against Centralized Regulation– Finally, cryptocurrency is a bet against centralized monetary regulation. Many ask, “are cryptocurrency exchanges regulated?” The answer is largely no. While in very few countries there is some regulation as it is looked at as a commodity, there are key differences in the regulation surrounding regular currency and the regulation surrounding cryptocurrency. At the end of the day, cryptocurrency is largely untraceable, giving the miner a bit of privacy in how much money they are making and what they are doing with that money

Source: https://www.invest.com/blog/news/benefits-cryptocurrency-mining/

FEW DISADVANTAGES OF MINING CRYPTOCURRENCY

Cryptocurrency mining, like any other high yield investment activity comes with its disadvantages.

. First comes the risk of depreciation. Just like any other asset, cryptocurrencies face the challenge of the risk of losing their value such that the value of the cryptocurrency you invested, instead of actually growing, drops over a certain time. In such as a case then the mining becomes a non-profitable activity to the miner. Companies that facilitate the mining would normally do away with the business at least till the business picks again or try working with currencies that have not been affected as much. Second comes the issue of electricity. The cost of electricity can certainly tamper with your earnings by the means of actually eating into them.

. Losing your digital wallet may also be a risk that one may encounter if not careful. This happens in the case where one is locked out in the case of forgetting your wallet’s password. Another case is when the wallet provider happens to run out of business. The sad news, unfortunately, is that one cannot recover his or her wallet once locked out. This is all due to the fact that the system that manages cryptocurrency mining like the bitcoin mining, is the decentralized kind of system. Coins that happen to be in such wallets get entirely lost from the economy. Aside from that, there is the issue of hackers breaking into and emptying your wallet.

.Another challenge could be the issue of fraudulent organizers. It is no new news to here of cases of dishonest organizers managing mining pools. Dealing with such is putting your earnings at risk. What happens if you unknowingly engage in a mining group whose administrators are dishonest fellows is that they get to eat up coins that you have earned. That is not all. In worst cases, such fraudsters can go as far as taking all your earnings from your wallet altogether. This risk, fortunately, has a solution. Engage yourself with a mining company that is already established in this investment sector and one that certainly has a good reputation.

source :https://medium.com/@valhallamining12/disadvantages-of-cryptocurrency-mining-900ffc29c64e